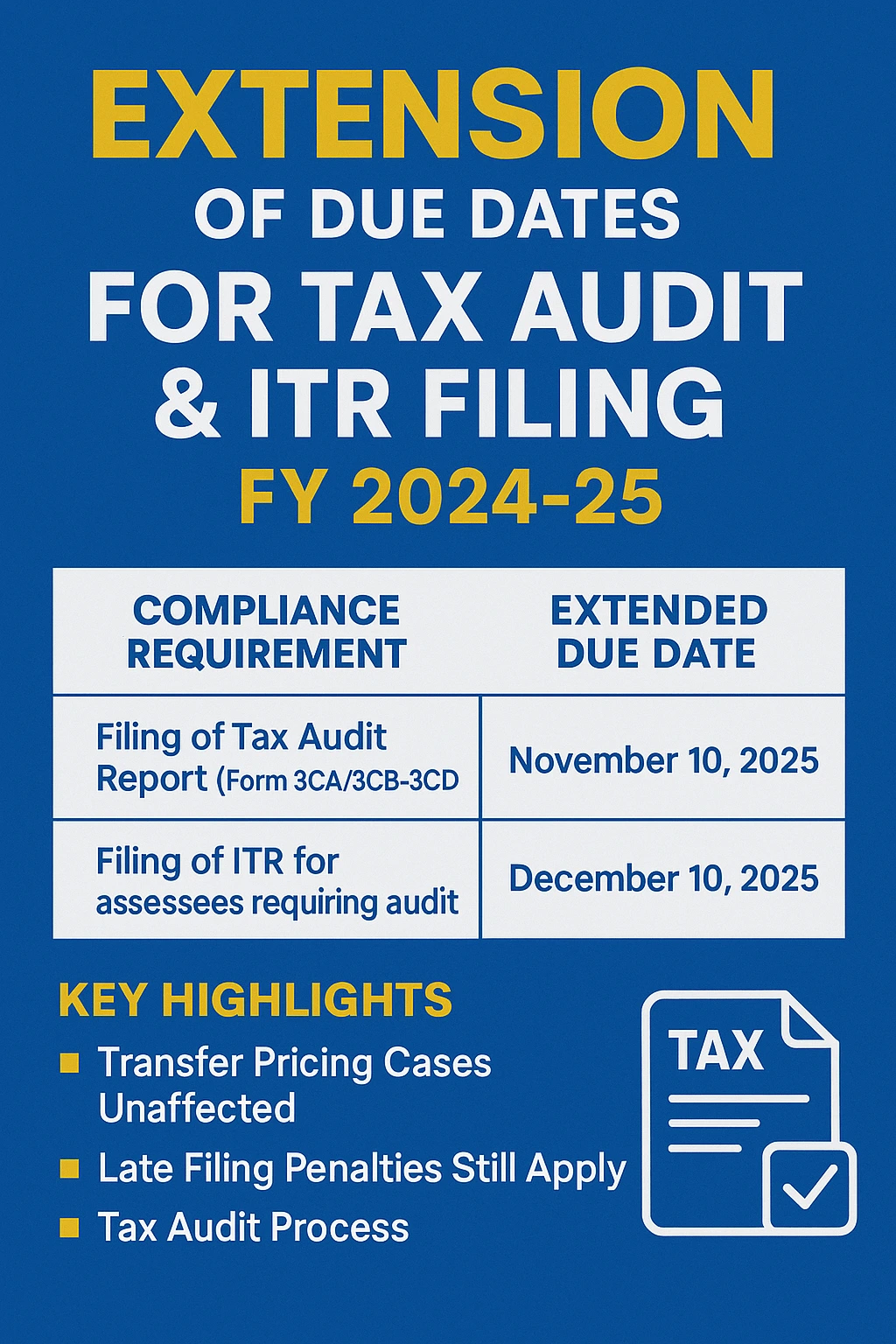

A relief for taxpayers and tax professionals — revised timelines for audit reports and ITR submissions (AY 2025–26).

Revised Due Dates

| Compliance Requirement | Extended Due Date |

|---|---|

| Filing of Tax Audit Report (Form 3CA / 3CB–3CD) | November 10, 2025 |

| Filing of Income Tax Return (ITR) — assessees requiring audit | December 10, 2025 |

Key Highlights of the Extension

- Transfer Pricing Cases Unaffected:

For assessees required to furnish a report under Section 92E (international or specified domestic transactions), the ITR filing due date remains November 30, 2025. - Late Filing Penalties Still Apply:

CBDT has clarified that filing after the revised deadlines will attract penalties:- Up to ₹5,000 as a late filing fee;

- Reduced fee of ₹1,000 where total income does not exceed ₹5 lakh.

Interest for delayed tax payments may also be levied as per applicable provisions.

- Tax Audit Process:

The tax audit report must be uploaded on the Income Tax Department e-filing portal by a Chartered Accountant. The assessee must then review and accept the uploaded audit report in their e-filing account before the ITR can be filed.

Note: Transfer pricing assessees should continue to follow the earlier date (Nov 30, 2025) for ITR filing — the extension does not apply to Section 92E cases.

Why the Extension Matters

The extension offers additional time to complete detailed audit procedures and reduces the pressure of overlapping statutory deadlines. This helps improve accuracy in filings and gives chartered accountants and finance teams room to finalize records without compromising compliance.